01 Mar 2014 ObamaCare Exchanges: Less Choice, Higher Prices

Executive Summary

Many supporters of ObamaCare insisted that the health insurance exchanges created by the law would result in consumers having a greater choice among insurance policies and lower prices.

This study tests those claims by examining policies on the exchanges in metropolitan areas across 45 states for a single 27-year-old and a 57-year-old couple. It then compares those with the policies available in those same areas on eHealthInsurance.com (eHealth) and Finder.healthcare.gov (Finder) in 2013.

The results show that the claims that the ObamaCare exchanges would offer greater choice and lower prices did not hold up. A 27-year-old male had, on average, ten more policies to choose from on eHealth versus the exchange and 31 more on Finder. A 27-year-old female had an average of ten more insurance options on eHealth and 38 on Finder. There were an average of nine more policies on eHealth and 19 more on Finder for a 57-year-old couple.

Across all areas examined, the exchanges have resulted in a substantial reduction in choice. For 27-year-olds, there were 442 fewer policies on the exchanges versus eHealth, a drop of 18 percent. There were 1,306 fewer policies on the exchange versus Finder for 27-year-old males and 1,716 fewer for females, declines of 38 percent and 46 percent, respectively. For 57-year-old couples, there were 406 fewer policies on the exchanges compared to eHealth and 855 fewer versus Finder, drops of 18 percent and 31 percent, respectively.

Consumers also previously had more lower-cost options than they now have on the exchanges. A 27-year-old male had, on average, access to 32 policies on eHealth that cost less than the cheapest policy on the exchanges and 38 policies that cost less on Finder. There were an average of 18 cheaper policies on eHealth and 20 on Finder for a 27-year-old female. A 57-year-old couple had access to an average of 29 cheaper polices on eHealth compared to the lowest-cost policy on the exchange and 28 on Finder.

An examination of subsidies that consumers can receive to purchase insurance on the exchanges produced mixed results on costs. A 57-year-old couple earning $50,000 annually was usually eligible for a subsidy large enough that the price of the cheapest exchange policy was lower than the price of any policy on eHealth or Finder. But for a 27-year-old earning $25,000 annually, the subsidy was less potent. In fact, even after subsidy options were accounted for, 27-year-old males still had access to an average of 18 cheaper polices on both eHealth and Finder, while a 27-year-old female had access to an average of nine on eHealth and eight on Finder.

Introduction

The ObamaCare exchanges are online marketplaces where consumers can shop for and purchase insurance. Consumers whose income is low enough can receive a tax-supported subsidy to help pay the premium.

Prior to the exchanges, consumers without access to employer-based coverage often purchased insurance on the individual market in the state in which they lived. Supporters of ObamaCare have made grandiose claims about the options consumers have while shopping for insurance polices on the exchanges. They stated there would be a greater choice of plans on the exchanges and that plans would cost less compared to the individual market:

• During a November 2013 press conference, President Obama claimed that on the exchanges consumers “have more choice, they’ll have more competition. They’re part of a bigger pool. The insurance companies are going to be hungry for their business. So the majority of folks will end up being better off.”1

• In a 2012 Meet the Press interview, House Minority Leader Nancy Pelosi (D-CA) said, “Everybody will have lower [insurance] rates.”2

• Ezra Klein, then of the Washington Post, argued in 2009 that the exchanges would be dynamic:

And what happens when you introduce productive competition, efficiencies of scale, more innovation and increased consumer power into a market as dysfunctional as the current situation for health insurance? In theory, you get lower prices and higher quality. And if the Health Insurance Exchange has lower prices and higher quality, more individuals will use it and more companies will buy into it. And if that happens, then the efficiencies of scale should increase, and so should the pace of innovation (as the rewards will be greater with more customers), and so the Health Insurance Exchange should further outpace the other markets, thereby attracting yet more customers, thereby further accelerating the virtuous cycle. Eventually, it could become the country’s primary insurance market.3

Do the exchanges offer a greater choice of insurance policies than the individual market had in 2013? And do they have policies that cost less than those that were on the individual market prior to the exchanges?

This study puts those claims to the test by comparing the exchanges with the policies available in 2013 on two websites, eHealthInsurance.com (“eHealth”) and Finder.healthcare.gov (“Finder”). Both eHealth and Finder were easily accessible to consumers, enabling them to shop for policies, compare benefits and premiums and sign up for policies online.

This study builds on a previous study conducted by the U.S. Department of Health and Human Services that examined the lowest-price policies on the 36 federal exchanges for both a hypothetical single 27-year-old who did not receive a subsidy and a hypothetical single 27-year-old who earns a low enough income ($25,000 annually) to qualify for a subsidy to put toward the purchase of insurance.4

This study compares the number of policies available to a single 27-year-old on the exchanges versus eHealth and Finder. It also examines if policies on eHealth and Finder cost less than the lowest-cost policy on the exchange for a single 27-year-old who pays full price on the exchange and for one who has access to a subsidy. It expands the number of exchanges examined to 45: 34 run by the federal government, ten run by state governments, and one run by the municipal government of Washington, D.C.

This study also includes a hypothetical 57-year-old couple that receives no subsidy and one that earns $50,000 annually, an income low enough to qualify for a subsidy. It compares both the number of policies and the lowest-cost policies for these couples on the exchanges versus those on eHealth and Finder. Both the 27-year-old single person and the 57-year-old couple are assumed to be without dependent children.

Jim Bulger

“The deductible in our plan was high,” said Jim Bulger, “but it kept the premium reasonable. Plus, we’re pretty healthy, so it worked for us.”

Bulger is 46 and runs a cattle association in San Antonio, Texas. He has two sons, ages 18 and 15, for whom he must provide health insurance. Until last year he had a Humana One Enhanced plan that had monthly premium of $298 and an individual deductible of $5,000.

Early in October 2013, Jim found himself in the same position as roughly 5 million other Americans who purchased their insurance on the individual market. He received a letter from his insurer informing him that his policy would be discontinued after December 31, 2013 because it did not meet the standards under ObamaCare.

Humana offered Jim a new plan that was similar to his old one but now had additional benefits that met the new ObamaCare standards. Jim chose the plan because he liked the service he had received from Humana over the years and it would be easier to keep his doctor. Yet the new policy costs $549 per month with a $3,500 deductible.5 He earns too much to qualify for a subsidy, and the extra $251 he must pay each month does not please him.

“The $298 I paid for the other policy, that fit my budget very well,” he said.

He pays extra for benefits he doesn’t need. He has no plans to have more kids, so he doesn’t need a maternity benefit.

“I’m mentally very healthy — so are my kids. No drugs, no problems with alcohol. I don’t need the mental health benefit,” Jim said.

On the exchange, he has a choice of 58 plans. The cheapest policy, a Blue Advantage Bronze HMO 005, has a monthly premium of $366 with a $6,000 deductible. On eHealth, Jim would have had 82 plans to choose from. Fourteen of them had premiums less than $366 a month with deductibles of $5,000 or less. But most of those policies were discontinued at the end of 2013.

Jim considered going without insurance and just paying the fine under ObamaCare’s individual mandate. In the first year, that could cost him about $800.6

“$800 annually versus paying between $500 and $600 a month? If I didn’t have to insure my kids, yeah, I’d probably go without insurance,” he said.

Although Jim is angry at losing his insurance, he is somewhat subtle when discussing ObamaCare.

“I really hate it!” Jim said. “My rates are going up so the system can take on people who were denied insurance. Plus, I’ve got to pay taxes to subsidize people on the exchange. So my rates are going up and I get to pay the taxes — I’m getting screwed.”

Comparing Markets

This study is more than just a comparison of websites. It is a comparison of less regulated markets (the state individual health insurance markets in 2013 of which eHealth and Finder were a part) and the more regulated markets of the ObamaCare exchanges.

The exchanges are governed by three regulations that were not present in most of the state individual markets: standardization of insurance plans, community rating and guaranteed issue. Six states that had community rating and guaranteed issue regulations in their individual markets in 2013 — Maine, Massachusetts, New Jersey, New York, Vermont, and Washington — were excluded from this study.

ObamaCare standardizes plans on the exchanges by establishing five levels of coverage, limiting their out-pocket costs, prohibiting annual or lifetime limits, and requiring plans to cover ten “essential health benefits.” The exchanges establish four levels of coverage — bronze, silver, gold and platinum. Each level offers more coverage than the last by lowering out-of-pocket costs and increasing premiums, with bronze offering the least coverage and lowest premiums.7 There is one other level, known as “catastrophic,” which has even less coverage and usually costs less than bronze policies. Catastrophic policies are only available to consumers who are between the ages of 18-29. No subsidy is available to someone who chooses a catastrophic policy.

No plan for a single person on the exchange can have a deductible or total out-of-pocket costs higher than $6,350 in 2014. Insurers can no longer offer plans with annual or lifetime limits, as ObamaCare phased out such limits over a number of years. ObamaCare prohibited the last of these limits, an annual limit of $2 million, beginning on January 1, 2014.

Finally, all plans must cover ten “essential health benefits,” including ambulatory patient services, emergency services, hospitalization, maternity and newborn care, mental health and substance use disorder services, prescription drugs, rehabilitative and habilitative services and devices, laboratory services, preventive services, and pediatric services.8

Strict community rating proscribes insurers from adjusting premiums to match any of a consumer’s risk factors, such as health status, gender, age or tobacco use. The ObamaCare exchanges use a somewhat less restrictive form of community rating. It prohibits insurers from underwriting on the basis of an individual’s health status or gender, but they can underwrite for tobacco use. For age, insurers must use an “age rating band” of one to three — that is, the oldest person on an exchange can’t be charged more than three times that of the youngest person. Prior to ObamaCare, most individual markets had a broader age rating band of 1 to 5.9

Guaranteed issue is a regulation that requires an insurer to sell a policy to any individual regardless of health condition at any time. In the ObamaCare exchanges, guaranteed issue requires insurers to sell a policy to any individual but only during the annual open enrollment period which will usually run from October to December.

All of these regulations will impact the amount of choice and prices on the exchanges. Standardization seems likely to reduce the number of plans that consumers have access to on the exchanges when compared to the individual market. Standardization restricts the ability of insurers to offer a wider array of deductibles and out-of-pocket cost levels or to offer plans with annual or lifetime limits. It also restricts their ability to offer plans with differing levels of benefits. This could lead to fewer choices for consumers on the exchanges.

Community rating and guaranteed issue are likely to drive insurance prices higher. These regulations require insurers to take on substantial risk without knowing in advance what those risks are. Guaranteed issue forces insurers to take all comers regardless of health conditions. Community rating prohibits them from taking health-status into account when adjusting the premium. This makes it far more difficult for insurers to project what their costs will be. As a result, insurers are more likely to charge higher prices to cover their costs.

Standardization also puts upward pressure on prices. Insurers can lower the price of their policies by offering policies with higher deductibles and out-of-pocket costs, with annual and lifetime limits or with fewer benefits. By taking those options away, the ObamaCare exchanges restrict the ability of insurers to lower the prices of their policies.

History shows that higher premiums and less choice follow when legislatures impose community rating and guaranteed issue on state health-insurance markets. In the early 1990s the legislatures in eight states — Kentucky, Maine, Massachusetts, New Hampshire, New Jersey, New York, Vermont and Washington — passed some form of these regulations. In the four years after New York imposed community rating and guaranteed issue, several major insurers increased their rates by 35 to 40 percent. In 1998, several insurers requested rate increases between 50 and 80 percent to stem rising losses. The state government only permitted them rate increases of 10 percent.10

After Kentucky imposed community rating and guaranteed issue in 1994, an estimated 850,000 people in the individual market saw substantial hikes in their health insurance rates.11 The number of policies also dropped as over 40 insurers left Kentucky’s individual market by 1998 in response to the new regulations. Indeed, by the late 1990s only two companies were still selling policies in the individual market.12

Kentucky was one of two states listed above (the other being New Hampshire) to eventually repeal community rating and guaranteed issue. Some competition did return as Kentucky had six companies selling policies in the individual market as of 2011.13 But its individual market was never as vibrant as it was in the early 1990s before community rating and guaranteed issue were imposed.

It is possible, however, that the ObamaCare exchanges will not repeat history. The exchanges offer some consumers subsidies, something that none of the eight states mentioned above did. Specifically, everyone who makes between 138 percent of the federal poverty level (FPL) and 400 percent FPL in a state that has expanded Medicaid and between 100 percent FPL and 400 percent FPL in a state that did not expand Medicaid is eligible for a subsidy to help pay for insurance on the exchange. Because of the way the subsidy is calculated, not everyone who makes less than 400 percent FPL will qualify for a subsidy.14 Nevertheless, data on exchange enrollment through December show that nearly 80 percent of enrollees have qualified for a subsidy.15 The subsidies could help drive net insurance prices lower for many enrollees compared to what they might have paid on the individual market in 2013.

The subsidies might also boost the amount of choice on the exchanges. Insurers will no doubt want to get the subsidies being funneled through the exchanges. This might incentivize them to offer many choices to consumers on the exchange, possibly leading to more insurance options than existed in 2013 on sites such as eHealth and Finder.

Choice

The Heritage Foundation’s Ed Haislmaier has examined the number of insurers participating in the exchanges. His research suggests that choice of insurance will decline under ObamaCare. In 39 states and the District of Columbia there were more insurers participating in the individual market in 2013 than there were insurers participating in the exchanges. In total, there were 360 insurers in the state individual markets versus 254 in the exchanges.16 The decline in insurers likely means a decrease in the number of insurance policies.

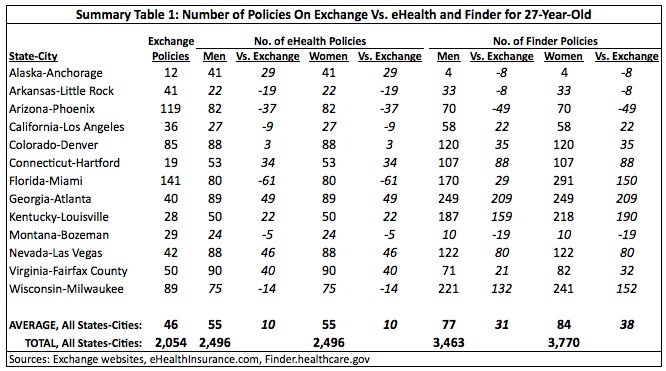

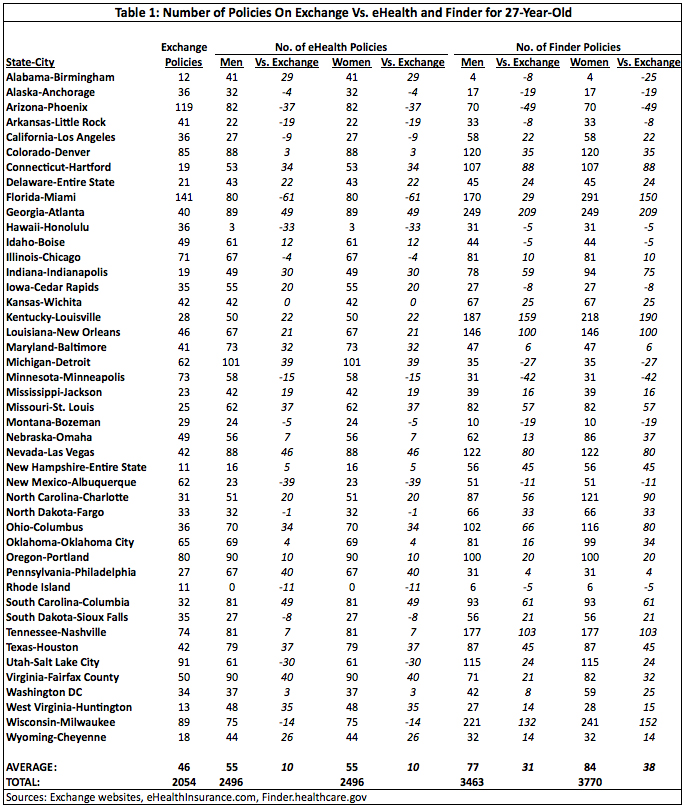

The data here reveals that there was an overall decrease in the number of policies. As Summary Table 1 shows, 27-year-olds in most areas had considerably more options on eHealth and Finder than they do now on the exchanges. (Full results for all tables are available in the appendix at the end of the study.) In 30 of the 45 areas examined, eHealth had more policies than the exchange. Finder had more policies than the exchange in 33 areas.

The average shows that eHealth exceeded the exchanges in the number of polices by ten for both men and women, and Finder had 31 more policies for men and 38 more for women compared to the exchanges. Across all areas, there were 442 fewer policies available for both men and women on the exchanges than on eHealth, a drop of 18 percent. There were 1,306 fewer policies for men and 1,716 fewer policies for women on the exchanges compared to Finder, declines of 38 percent and 46 percent, respectively.

Atlanta, Georgia saw the largest drop in choice for 27-year-olds, with eHealth having 49 more polices and Finder having 209 more policies than the exchange. The greatest gain in choice was found in Phoenix, Arizona, where the exchange had 37 more policies than eHealth and 49 more than Finder.

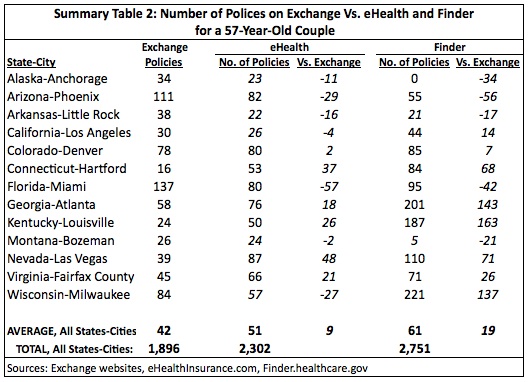

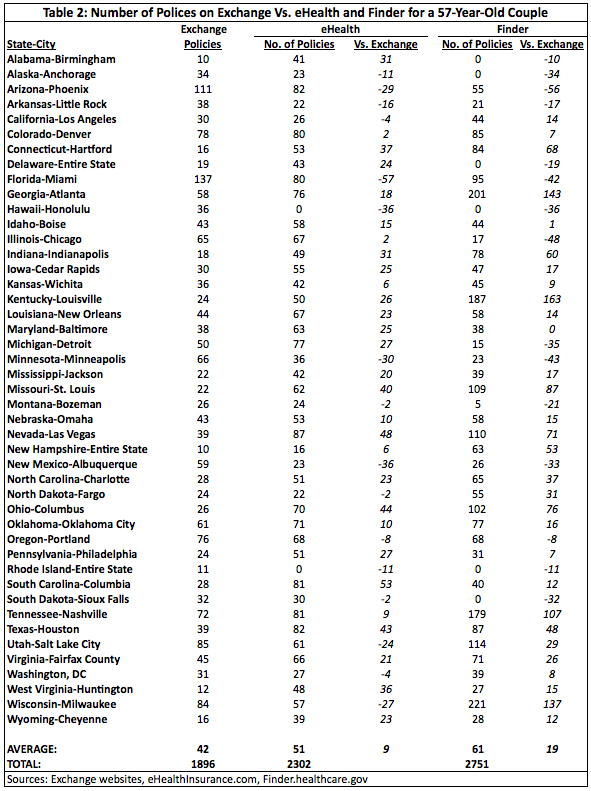

The results for a 57-year-old couple show a similar decline in choice. In 31 municipal areas eHealth had more policies than the exchange. Finder had more policies in 30 areas.

As Summary Table 2 demonstrates, the average number of policies by which eHealth exceeded the exchange was nine and was 19 for Finder. In total, there were 406 fewer policies on the exchange versus eHealth versus the exchange and 855 fewer versus Finder for a 57-year-old couple, declines of 18 percent and 31 percent, respectively.

A 57-year-old couple in Louisville, Kentucky saw the greatest loss of choice, with eHealth having 26 more policies than the exchange and Finder having 163 more. A Miami, Florida couple saw the greatest increase in insurance options with the exchange exceeding eHealth by 57 policies and Finder by 42.

Prices

In an extensive examination of the insurance prices on the exchange and in individual markets prior to the exchanges, the Heritage Foundation found that the price of insurance would be more expensive on the exchanges in 45 states and the District of Columbia. While some of the increases in premiums were small, many were 50 percent or higher. In about nine percent of the cases the premiums would more than double.17

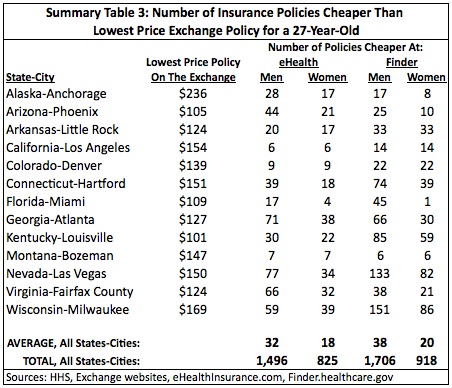

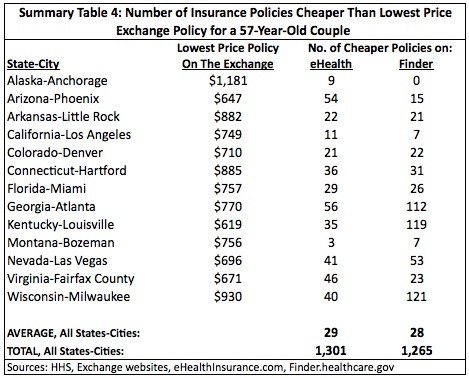

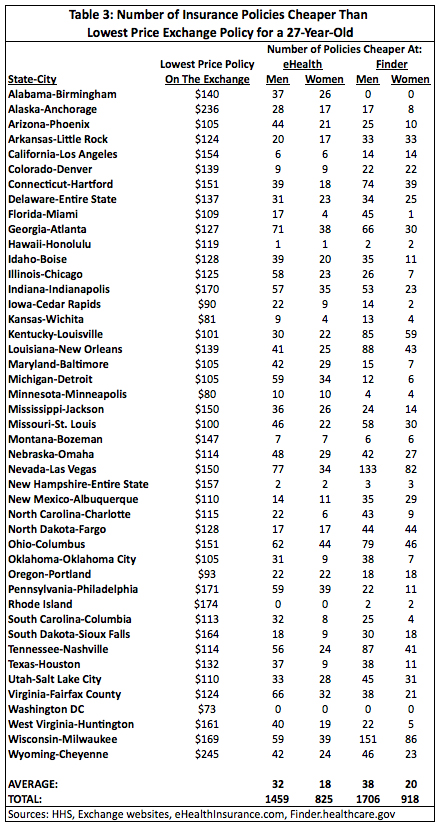

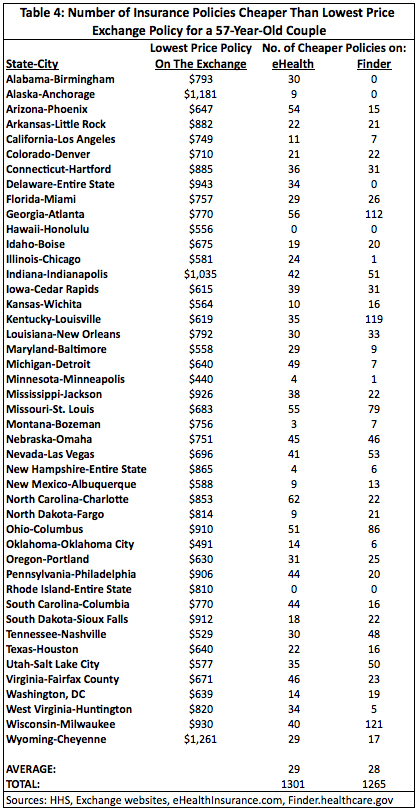

The data here strengthens the case that insurance was cheaper prior to the exchanges. Both Summary Tables 3 and 4 show that there were many insurance options on eHealth and Finder that cost less than the cheapest policies on the exchange. A 27-year-old male who paid full price on an exchange (i.e., he did not receive a subsidy) had, on average, 32 cheaper policies to choose from on eHealth and 38 on Finder. For a 27-year-old female eHealth had, on average, 18 cheaper polices and Finder had 20 cheaper policies compared to the exchanges. A 27-year-old living in Las Vegas, Nevada seemed the most likely to experience a price increase going to the exchange as there were 77 cheaper policies on eHealth and 133 on Finder for a male and 34 cheaper polices on eHealth and 82 on Finder for a female. Only Washington, D.C. had no policies on either website that cost less than the cheapest exchange policy.

Of course, these tables only show how many lower price policies were available on eHealth and Finder to people who paid full price on the exchange. Would a person who received a subsidy on the exchange have any cheaper options on eHealth and Finder?

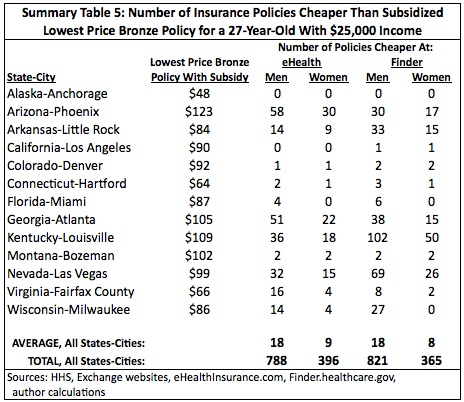

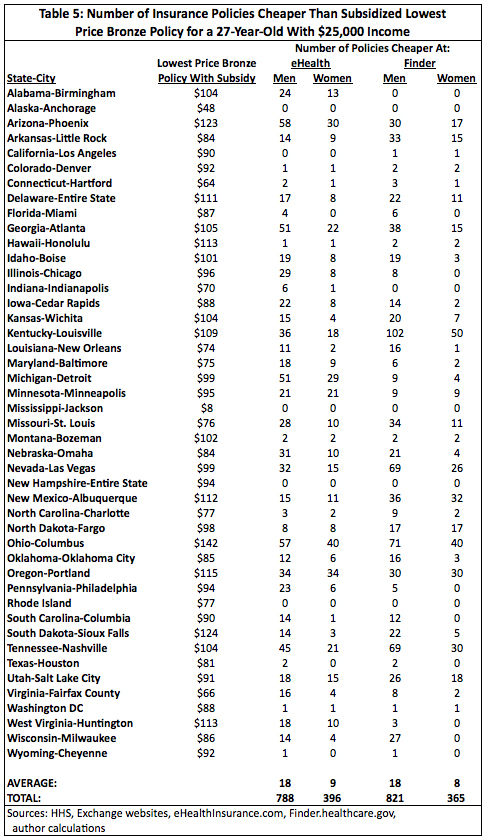

To answer that, this study examined the price 27-year-olds earning $25,000 annually and 57-year-old couples earning $50,000 annually would pay for insurance on the exchange. It compared the price of policies on eHealth and Finder to the price of the lowest-cost bronze policy with a subsidy. Summary Table 5 displays some of the results for 27-year-olds. Surprisingly, most areas examined had at least a few policies that were cheaper on either eHealth or Finder than the lowest-cost bronze policy with a subsidy. Some had a substantial number. EHealth had 57 cheaper polices for a male and 40 for a female in Columbus, Ohio. Men in Louisville, Kentucky had 102 cheaper polices on Finder and women had 50. Only four areas — Anchorage, Alaska, Jackson, Mississippi and the states of New Hampshire and Rhode Island — had no policies on either website that were cheaper. For a 27-year-old male earning $25,000, the average number of policies cheaper than the lowest price bronze policy with a subsidy was 18 on both eHealth and Finder. For a female, the averages were nine on eHealth and eight on Finder.

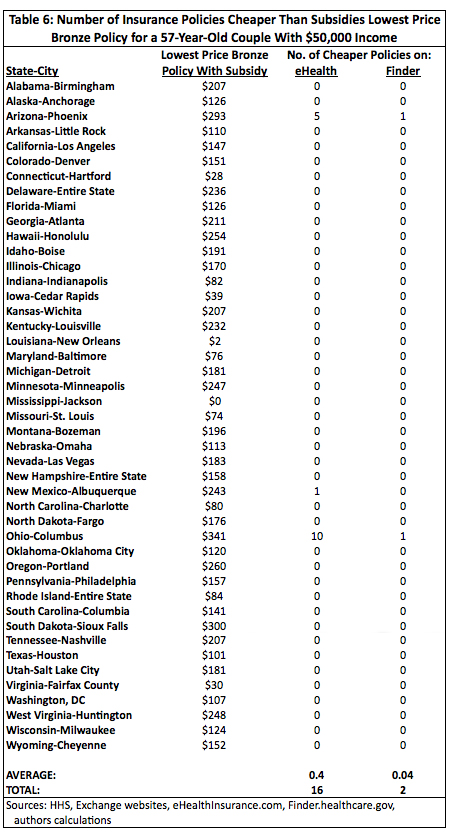

For a 57-year-old couple earning $50,000 annually the results were so uniform as to make a summary table moot. In all but three areas — Phoenix, Arizona, Albuquerque, New Mexico, and Oklahoma City, Oklahoma — there were no policies on either eHealth or Finder that cost less than the cheapest bronze policy with a subsidy. This is not that remarkable since, as other research has shown, the method for calculating subsidies results in much larger subsidies for older people on the exchanges than for younger people.18 In the exchanges examined here, the average subsidy for a 27-year-old was $70 per month while it was $599 per month for a 57-year-old couple.

Critics may point out that not every person who applied for coverage via eHealth or Finder received coverage at the prices listed on those websites. For example, the CoreShare 5000/50% policy from Anthem Blue Cross Blue Shield that was available to a 57-year-old couple in Milwaukee, Wisconsin cost about $501 per month. However, 23 percent of people who applied were offered the policy at a higher rate (a “surcharge”) while 12 percent were turned down for the policy.

There are three responses to this. First, 75 percent of those who applied for this policy received it at the advertised rate. Those people would see a substantial premium increase if they had to give up their policy and purchase insurance on the exchange. Second, even people who received a surcharge could easily pay more on the exchange. A couple who paid a 50 percent surcharge on a CoreShare 5000/50% policy would pay a premium of about $751 per month. That’s still less than the $930 premium for the Anthem Bronze DirectAccess plan, the cheapest plan on the federal exchange for Milwaukee.

Finally, Avik Roy of the Manhattan Institute has conducted research that accounts for both surcharges and denials. In 72 percent of the cases he examined, premiums in the exchanges still exceeded those on state individual markets.19

Conclusion

The claims by ObamaCare supporters that the ObamaCare exchanges would result in greater choice of policies and lower premiums are not supported by the evidence. This study shows that consumers were much more likely to have more insurance options on eHealth and Finder than on the exchanges. They also had access to many plans that cost less than the cheapest plans on the exchanges. That holds true not only for those who have to pay full price on the exchange but even for some who have access to subsidies.

That is the predictable result of regulations that standardize plans and impose community rating and guaranteed issue. Indeed, in the years to come, community rating and guaranteed issue will likely lead to even higher premiums and less choice on the exchange. History shows that community rating and guaranteed issue often lead to the “death spiral” of a health insurance market. A death spiral occurs when the young and healthy drop out of the “insurance pool.” This leads to “adverse selection” in which insurance is primarily attractive to those who tend to be older and sicker. If the insurance pool is comprised largely of older and sicker people, then insurance prices naturally rise to cover their costs. That rate increase results in even more young and healthy people dropping their insurance, leaving the pools even older and sicker than before, and so forth.

As the insurance pool becomes smaller and more expensive to cover, many insurers face huge losses. Eventually, they exit the market, which leaves, at most, a few large insurers still doing business. Fewer insurers in the market means a reduction in insurance options for consumers.

ObamaCare’s exchanges have already taken their first steps toward a death spiral. The Obama Administration estimates that 38 percent of the exchange insurance pool must comprise of 18-to-34-year-olds to prevent a death spiral. Thus far, 25 percent of exchange enrollees are aged 18-34.

Worse, enrollees’ choice of insurance suggests that the pool may be sicker than is optimal for an insurance pool. Sixty-two percent of exchange enrollees have chosen a silver plan. For enrollees at or below 250 percent FPL, silver plans tend to offer the most coverage for the lowest price. For persons under 250 percent FPL, ObamaCare offers help with copays and deductibles, but only if the consumer chooses a silver plan. The actuarial value for a silver plan is 70 percent (that is, a silver plan must, on average, cover 70 percent of a policyholder’s medical claims), but when the subsidies for cost-sharing are included, the actuarial value rises to between 73 and 94 percent.20 As one writer notes, “Why would someone opt for a silver-level plan over a cheaper bronze or catastrophic-level plan? The most plausible explanation is that the enrollee anticipates incurring significant medical expenses over the coming year, which is to say that he’s not healthy.”21

One provision of ObamaCare known as a “risk corridor” may mitigate the death spiral. The risk corridor requires insurers that make a profit on the exchanges and the taxpayers help offset some of the costs of those insurers who incur losses on the exchanges. However, the risk corridor expires in 2017. After that, chances are that the descent of the exchanges into higher insurance prices and less choice will accelerate.

Methodology

1. Data from eHealthInsurance.com for a 27-year-old single person downloaded between Sept. 30, 2013 to Oct. 22, 2013. Data from Finder.healthcare.gov 27-year-old single person downloaded between Nov. 11, 2013 and Nov. 15, 2013. Data for both eHealthinusarance.com and Finder.healthcare.gov for a 57-year-old couple downloaded between Nov. 27, 2013 and Nov. 30, 2013. EHealthInsurance.com did not have policies for Rhode Island. This was counted as “zero” in the study — that is, eHealthIinsurance.com had zero policies for a 27-year-old male in Rhode Island. Alabama and Alaska were missing from the data for Finder for a 57-year-old couple. Although the later date that the data was collected probably explains why those two states did not appear for a 57-year-old couple, this study assumed that such policies were not available for those two states for a 57-year-old couple. As such, the number of policies were also counted as “zero” in the study.

2. On Finder.healthcare.gov, if “Policy B” had the same benefits as “Policy A” except that Policy B also offered maternity benefits, Finder.healthcare.gov counted this as two policies. This study counted that as only one policy for a 27-year-old single male and a 57-year-old couple, since it is unlikely either would have use for maternity benefits.

Data Sources

Federal Exchanges: HHS, “Health Insurance Marketplace Premiums for 2014,” http://aspe.hhs.gov/health/reports/2013/marketplacepremiums/ib_marketplace_premiums.cfm, and https://www.healthcare.gov/find-premium-estimates/.

State Exchanges: Data from state exchanges found at:

California: https://www.coveredca.com/shopandcompare/

Colorado: https://prd.connectforhealthco.com/individual

Connecticut: https://www.accesshealthct.com/AHCT/FamilyInformation.action?activetab=health Hawaii: https://www.connecthawaii.com/web/guest/premium-assistance-calculator

Kentucky: https://kyenroll.ky.gov/PreScreening/YouandYourHouseHold, Office of Kentucky Health Benefit Exchange, http://www.healthsherpa.com/

Maryland: http://www.healthsherpa.com/

Minnesota: https://plans.mnsure.org/mnsa/planadvisor/plan_advisor.htm

Nevada: https://www.nevadahealthlink.com/Individual.Anonymous/FindAPlan

Oregon: https://www.coveroregon.com/individual/browse

Rhode Island: http://www.healthsourceri.com/tools/calculate-your-savings/

Washington, D.C.: https://www.dchealthlink.com/browse-plans.

David Hogberg, Ph. D., is senior fellow for health care policy at the National Center for Public Policy Research.

Footnotes:

1 Ashley Kilough, “Obama apologizes for insurance cancellations due to Obamacare,” CNN, November 7, 2013, at http://www.cnn.com/2013/11/07/politics/obama-obamacare-apology/ (January 20, 2104).

2 “Nancy Pelosi Promises Lower Premiums for Everyone,” July 1, 2012 at http://www.youtube.com/watch?v=QqONZAN_Us0 (January 20, 2014).

3 Ezra Klein, “Health Insurance Exchanges: The Most Important, Undernoticed Part of Health Reform,” The Washington Post, June 16, 2009, at http://voices.washingtonpost.com/ezra-klein/2009/06/health_insurance_exchanges_the.html (January 22, 2014).

4 U.S Dept. of Health and Human Services, Office of the Assistance Secretary for Planning and Evaluation, “Health Insurance Marketplace Premiums for 2014,” ASPE Issue Brief, September 2013, at http://aspe.hhs.gov/health/reports/2013/marketplacepremiums/ib_marketplace_premiums.cfm (September 29, 2013).

5 Jim’s new plan has a deductible of $3,500 for each person on the plan. The total deductible for his family is $7,000. His old plan had an individual deductible of $5,000 and a family deductible of $10,000.

6 Under ObamaCare’s individual mandate, people who don’t buy insurance must pay a penalty of $95 or one percent of their taxable income, which ever is greater. Bulger’s taxable income is in the range of $80,000. One percent of that is $800.

7 Each level of coverage has a different actuarial value. For example, a bronze plan has an actuarial value of 60 percent which means that the plan must cover, on average, 60 percent of a policyholder’s medical claims. The actuarial value for a silver plan is 70 percent, a gold plan is 80 percent and a platinum plan is 90 percent. A catastrophic plan does not have an actuarial value.

8 42 U.S.C. § 18022(b)(1)(A-J)

9 America’s Health Insurance Plans, Center for Policy and Research, “Age Rating,” no date listed, at http://ahip.org/Issues/Age-Rating.aspx (February 3, 2014).

10 Mark A. Hall, “An Evaluation of New York’s Reform Law,” Journal of Health Politics, Policy and Law, Vol. 25, No. 1, February 2000, pp. 84-85.

11 Conrad F. Meier, “Destroying Insurance Markets,” The Council for Affordable Health Insurance and The Heartland Institute, 2005.

12 Leigh Wachenheim and Hans Leida, “The Impact of Guaranteed Issue and Community Rating Reforms on Individual Insurance Markets,” Milliman, August 2007.

13 Ibid.

14 David Hogberg and Sean Parnell, “ObamaCare Exchanges: Just Because You Are Eligible For A Subsidy Doesn’t Mean You Will Qualify For One,” National Center for Public Policy Research, National Policy Analysis No. 653, September 2013, at https://nationalcenter.org/NPA653.html (March 1, 2014).

15 U.S. Department of Health and Human Services, Office of the Assistance Secretary for Planning and Evaluation, “Health Insurance Marketplace: February Enrollment Report,” February 12, 2014, at http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Feb2014/ib_2014feb_enrollment.pdf (February 12, 2014).

16 Edmund F. Haislmaier, “Health Insurers’ Decision on Exchange Participation: Obamacare’s Leading Indicators,” The Heritage Foundation, Backgrounder No. 2852, November 12, 2013, at http://www.heritage.org/research/reports/2013/11/health-insurers-decisions-on-exchange-participation-obamacares-leading-indicators (January 10, 2014). Also see Alyene Senger, “Lack of Competition in Obamacare’s Exchanges: Half of U.S. Has Two or Fewer Carriers,” The Heritage Foundation, Issue Brief No. 4802, November 8, 2013, at http://www.heritage.org/research/reports/2013/11/obamacare-insurance-exchanges-and-the-lack-of-competition (January 10, 2014).

17 Drew Gonshorowski, “How Will You Fare in the Obamacare Exchanges?” The Heritage Foundation, Issue Brief No. 4086, October 16, 2013, at http://www.heritage.org/research/reports/2013/10/enrollment-in-obamacare-exchanges-how-will-your-health-insurance-fare (October 18, 2013).

18 Hogberg and Parnell, September 2013.

19 Avik Roy, “Obamacare: Know Your Rates,” Manhattan Institute for Policy Research, no date listed, at http://www.manhattan-institute.org/knowyourrates/ (January 14, 2014); and Avik Roy, “Obamacare: Know Your Rates. Rate Change, Subsidy Beneficiaries, and More,” Manhattan Institute for Policy Research, no date listed, at http://www.manhattan-institute.org/knowyourrates/about.htm (January 14, 2014).

20 Edmund F. Haislmaier, “What the Obamacare ‘Death Spiral’ Debate Misses,” The Heritage Foundation, Commentary, January 29, 2014, at http://www.heritage.org/research/commentary/2014/1/what-the-obamacare-death-spiral-debate-misses (February 3, 2014).

21 Spencer Cowan, “The Obamacare Death Spiral Isn’t Dead,” The Weekly Standard, The Blog, January 16, 2014, at https://www.weeklystandard.com/blogs/obamacare-death-spiral-isnt-dead_774734.html (January 20, 2014).